The CCO as Closet CFO

Customer success is a revenue de-risking function, not a retention cost-center

This article is the first of three based on my conversation with Harini Gokul on the customer success function and its relationship with the CFO. Check out the discussion on Youtube and other episodes from Speaking C-Suite via the links below.

The reframe: CCO as revenue de-risking partner

There’s a real contrast in scaling a company at $50MM ARR versus $1B: at $50MM you can lose 20% of your customers and grow successfully through it, the acquisition is achievable. At $1B you can’t. The customer success function that worked through the first hundred million breaks at an order of magnitude more. As part of the Speaking C-Suite podcast series I interviewed Harini Gokul who spoke about how redesign of the customer success function is critical as the company scales. This article is the first of a series of three covering the concepts and insights that Harini shared in the discussion.

Harini’s philosophy is fundamentally that the CCO is the CFO’s revenue de-risking partner and should see themselves in a pseudo-CFO role, which she calls the Closet CFO. The CCO brings the most reliable, most forecast-able substrate of next year’s revenue. It’s way more impactful than just stating a retention rate would imply. (check out Harini’s interview with Churn.FM as well)

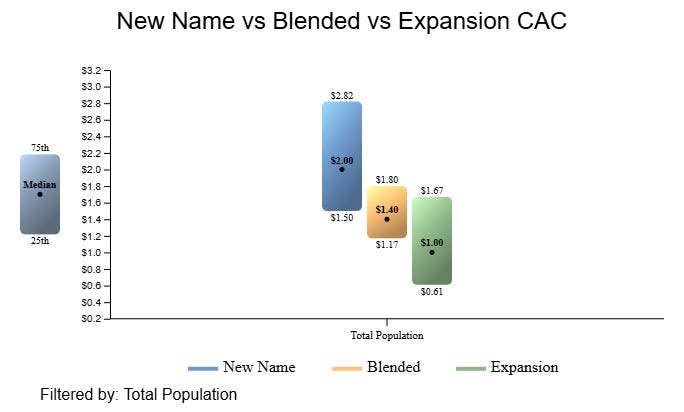

It is cheaper to sell to your existing customers as is shown in the chart from benchmarkit below. Said more technically, expansion CAC is lower than new CAC. It is clearly important to CFOs: lower acquisition investment leads to increased revenue from upsell and margin from uplift. With the right data its more predictable and a better overall capital return. A balance is of course essential, but it also helps identify issues with companies. For example, companies focusing on net-new CAC and, while still seeing top-line growth, what’s going on behind the scenes are declining retention metrics and a failing product and market vision overall. Net-new is a temporary band-aid.

The customer success team is the function closest to the customer. They see the expansion triggers and contraction signals way before anyone else. Integrate that contextual knowledge with solid data and usage monitoring and you have a very powerful customer evaluation framework. The recommendation then is for CCOs to run their function as a forecasting input, not a retention cost-center, as that is what is of most value to the CFO (or as Maxio outlines, companies should seek alignment between CS and the CFO).

The math: how the install base shrinks the net-new problem

Quantifying this in an example: Assume $1B target revenue, with a currently installed base of $400MM. A 90%+ GRR commitment de-risks $350MM before sales even has to touch a new logo. Or, every 1 percent of GRR at this scale represents $4MM of net-new sales the company doesn’t have to find and book. That increased retention leads directly to lower AE and SDR resourcing requirements—it directly affects net profitability. As a result GRR becomes a very powerful metric with indicators for both revenue growth and profitability.

Where this really shows up is in how the public markets value companies that vary across the NRR and GRR dimension (SaaSMag covers this well). You can distill things down to: A dollar of de-risked revenue is worth more than a probability weighted dollar of net-new revenue, even at the same nominal amount. Predictable revenue necessarily leads to a higher valuation multiple, it represents a more powerful company on paper. In the public markets revenue quality is priced explicitly, NRR and GRR are high up on the topic list in earnings materials and comps treat a 115% NRR business and a 100% NRR business as different categories of company. For private companies, this manifests itself in returns projections and working-capital planning. You can run a leaner company when the revenue base is reliable.

And at the board level, the CFO’s challenge is reduced, with a large segment of the revenue locked in at high confidence then the board and executives can focus on the more uncertain and variable component of net-new. Guaranteed to make you friends with your CFO.

Why every renewal must be a growth event

Every renewal must achieve expansion. Consider NRR and the magical pivot point of 100%. Below 100% and the company needs to add in new recurring revenue just to stay flat, you’re fighting to stay in the same place and as we cover in more detail below you’re spending more on acquisition per dollar of ARR when supplementing with new versus expansion. Above 100% and that company is successfully growing its existing customer base, and retaining that performance is compound growth. This is why Harini states the importance of renewal ARR increase “a flat renewal is a failed renewal”. Powerhouse growth comes from deepening the relationship and impact with your customers, demonstrating the product’s value continually over time and expanding scope of usage within the customer.

There’s a tendency to conflate the three main factors in renewal value: uplift, upsell and cross-sell. The first, uplift, is an increase in price for the same product or service—no change in what the customer is experiencing, just a capture of additional monetary value. The second, upsell, is an expansion of the product within the customer—additional seats, increased service capacity, more transaction volume etc. The customer is expanding their usage of the product. The third, cross-sell, is layering additional products or services into the relationship. New SKUs, services lines or similar to support different use cases.

A product with established foot-hold has pricing power. Even in this world of AI revolution it is still the case that enterprise environments have switching costs, and it is the imperative of the seller to monetize that latent value. Renewals have to be seen not as maintaining the status-quo, but as furthering the commitment of the customer to the product. Therein lies the secret to increased revenue and margin growth.

The cheapest dollar of growth on the P&L

It is striking how many companies only quantify and track new CAC and essentially ignore expansion CAC. As my discussion with Harini demonstrated, the margin growth opportunity with existing customers is a fundamental track to growth out-performing the market. There’s also no or proportionally lower integration or cost to deliver the expanded service. The customer is already on the product, using it and gaining the value-add experience.

Moreover, the expansion is forecast-able. Data available from customer usage gives clear indication on adoption and user dynamics that with the right assessment rubric can inform renewal and expansion selling conversations. Net-new by contrast relies on pipeline closing performance and is subject to sales-cycle timelines that can vary between prospects and also over time as the market evolves. Renewal timelines are transparent and very much under control of the company. CFOs can treat renewals as high-confidence whereas new-logo falls into wide-variance. This translates directly to working-capital planning and resourcing and eventually external valuation of the business model.

On every dimension relevant to the CFO, whether CAC, gross margin, predictability or capital efficiency, expansion is the preferable and better dollar for dollar. Companies as they scale past the product validation stage need to build out the customer success infrastructure to capitalize on existing customer dynamics.

The Closet CFO mindset

Underlying the whole thread here is a unique value represented by customer success and CCOs to CFOs: they bring the most secure and reliable source of revenue for upcoming periods. They are in a way, a CFOs greatest friend. And healthy companies will demonstrate good relationships between their CFO and CCO.

Aside from the technical details, and metrics recommendations embedded in here, that certainly should be a general takeaway: CFOs should look to CCOs as a key source of recurring revenue and cashflow, which provides the foundation on which to plan for upcoming periods. And CCOs should understand the value they present to the CFO and invest in that relationship to secure appropriate support and investment for maximizing the company’s growth potential.

In wrapping up, Harini suggests CCOs become “Closet CFOs”: the CCO should think and act like a CFO and in that way will build the most productive relationship with their CFO. Companies that achieve this integration in their exec team will capture the increased growth and margin opportunity and see that manifested in capital efficiency and valuation.

Look out soon for the second and third installments in this series on leadership in customer success!

AI’s Contribution

I wrote every word in this article. I like em-dashes. I do use Claude Code to help refine topic flow and structure plus research for articles.

Title and subtitle into ChatGPT for a “radical image”: